Prediction is very difficult, especially about the future.

Common quotation, variously attributed to Yogi Berra, Niels Bohr, Mark Twain and others.

Introduction

In Isaac Asimov’s famous science fiction novel Foundation, a group of scientists in the distant future led by Hari Seldon discover a mathematical method to predict the course of future events, anticipating the collapse of the reigning Galactic Empire into a new Dark Age. Armed with the mathematical methods of Hari Seldon’s “psychohistory,” the scientists create a Foundation on the edge of the Galaxy that saves civilization from the prophesied Dark Age. The notion that mathematics can be used to predict human behavior in economics, finance, politics, and many other fields and activities has great appeal. With the spread of increasingly powerful computers, complex mathematical models of economics, finance, and other human activities have become more and more common. Often, the motives are much less admirable than the selfless super scientists of Asimov’s tale. Often, too, the accuracy and performance of the mathematical models has been much less impressive than Asimov’s fictional new science of psychohistory.

In the last few years, complex models of the value of mortgage backed securities have proven disastrously incorrect, a major contributing factor to the Great Recession, the present financial crisis. This is only the latest in a succession of such failures in quantitative finance. Similarly, many sophisticated econometric models of the economy have proven unreliable. To the extent that these models are shaping public policy, personal and corporate investment decisions, and so forth, the pitfalls of mathematical modeling and seemingly abstruse issues in the philosophy of science such as Karl Popper‘s doctrine of falsifiability are having a substantial impact on people and society.

In fact, applying mathematical models to economics, finance, and other human activities is especially treacherous. All mathematical modeling suffers from the deep problem that one can construct an infinite range of functions that approximate current observations and data arbitrarily well and yet make any and all possible predictions about possible new observations. In practice, human beings use various criterion to select mathematical models that are likely to be true, many of which criterion cannot be justified in any rigorous or rational way and some of which criterion are difficult to identify (intuition, “that just doesn’t feel right”, “God doesn’t play dice with the universe.”). Nonetheless, human judgment has a high error rate, though surely much more accurate than a blind guess.

In addition to this pervasive problem, many of the assumptions used in applying mathematical models to physical processes such as the motion of the planets or radioactive decay surely do not apply to economics, finance, or other forms of human behavior. Our expectation is that the motion of the planets is governed by the same “laws” today as last year or last decade or in 1605 when Johannes Kepler first recognized the elliptical orbits of the planets. Indeed, this regularity of many natural phenomenon is strongly born out by experience. On the other hand, the economy or financial markets or other human activities change and evolve. However imperfectly, human beings learn from mistakes, develop new technologies and processes. Human beings are herd animals and prone to fads and fashions that have no parallel in physical phenomena. One would not expect the market for gold to be the same today as in 1960 and it was not. The price of gold was fixed by the US federal government in 1960 and today it is not.

This article takes a look at the price of gold since 1970 when the United States ended the gold standard. Gold is currently rising sharply in price as it did in the late 1970’s and early 1980’s. This article will show how it is possible to construct many different purely symbolic mathematical models of the price of gold that make different predictions. Indeed, one can cook up whatever prediction one would like. The article will also discuss the serious problems with applying the mathematical methods of physics and other “hard” sciences to the price of gold as a specific example of a general problem.

Mathematics for Goldfinger

With the collapse of the Bretton-Woods foreign exchange system (1968-1971), the price of gold, previously fixed to the US dollar, was allowed to float free. Since 1970 the price of an ounce of gold in US dollars has risen substantially.

Nominal Gold Price

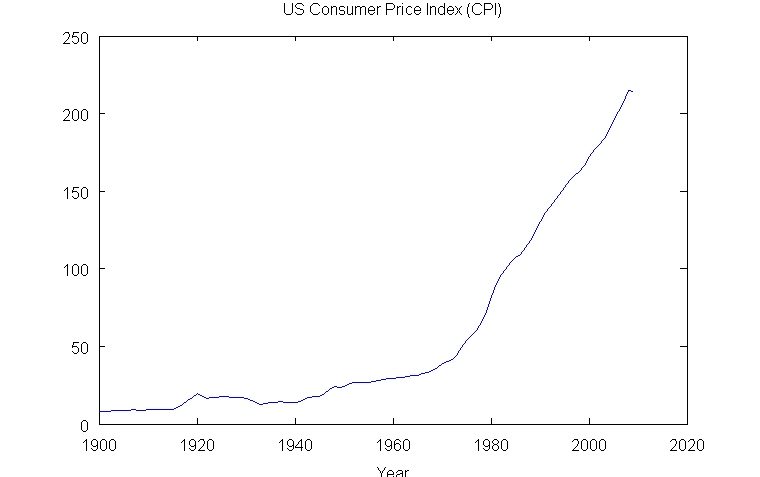

The United States government reports a consumer price index (CPI) that is purported to reflect the cost of living in US dollars for a typical US citizen. Although there are some reasons to be skeptical about the accuracy of the CPI in recent years, this article will use the CPI as a proxy for the overall price level in the United States.

United States Consumer Price Index

One can see that the CPI has generally risen at a higher rate since the United States ended the gold standard in 1970. This also corresponds to a period of overall rising energy prices and very limited progress in power and propulsion technologies. Many other areas have seen relatively limited scientific and technological progress during this period. Computers and electronics have, of course, continued their historical trend of rapid progress to the present.

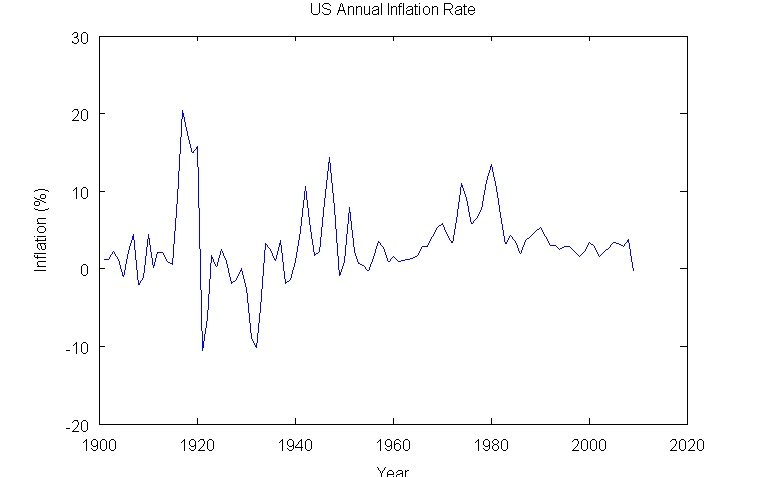

Historically, the US inflation rate was high during the periods of World War I and World War II, but otherwise generally lower than the present period, since 1970. The official inflation rate, the rate of increase of the CPI, was especially high during the 1970s, a period of sharp increases in nominal and real energy prices. The inflation rate derived from the CPI in recent years does not seem to reflect the common experience of rising energy prices since the late 1990s. Nor does it show any evidence of the sharp rise in housing prices in the US from 2002 to 2005; by many estimates, housing prices in urban areas remain high compared to the historical trend.

Inflation Adjusted Gold Price

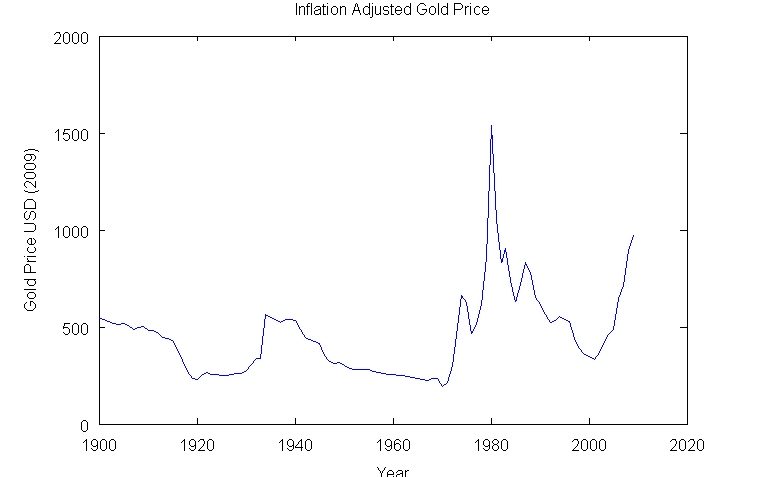

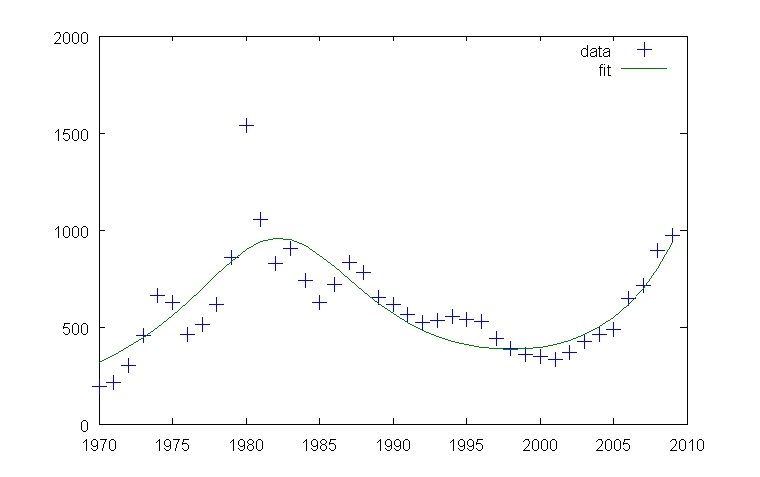

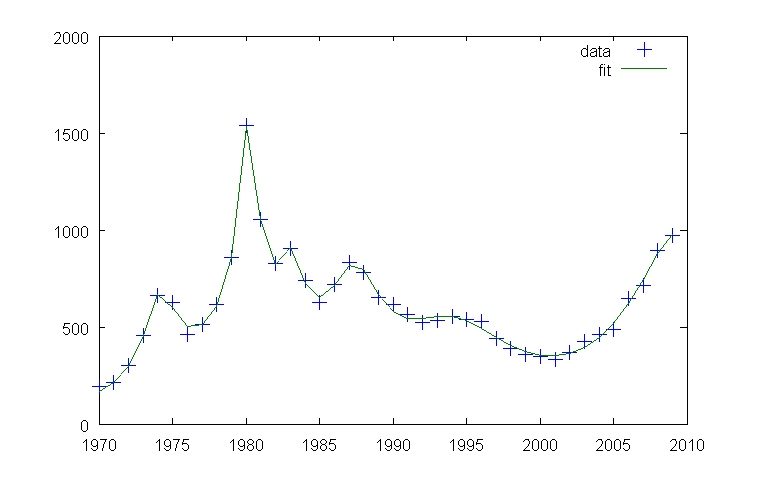

Investors are generally interested in the real inflation-adjusted value of an investment. The value of gold in real terms fluctuated somewhat during the period of the gold standard but has fluctuated much more since 1970. Particularly notable is the large spike in the real and nominal price of gold in the early 1980’s. In real terms, the current rise in gold price has not reached the level of the spike in the early 1980’s. If inflation has been higher than the official CPI, the current real price of gold would be even lower than the spike in the early 1980s.

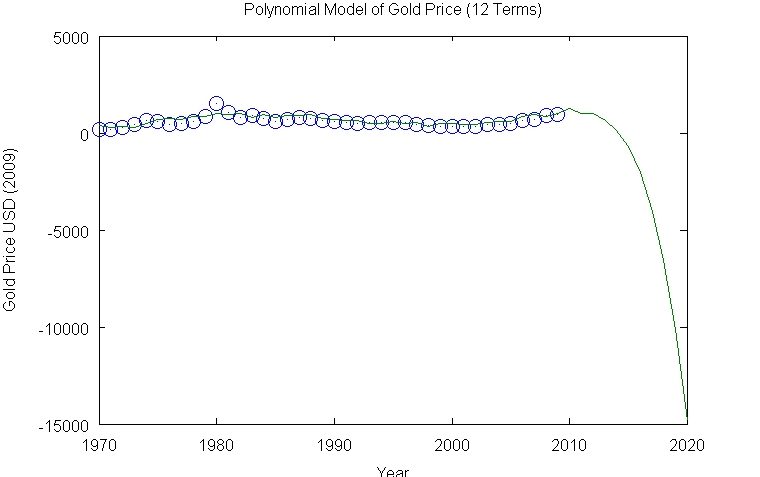

One can construct a simple symbolic mathematical model of the real price of gold since 1970 (the gold standard disintegrated between 1968 and August 1971 when the US government ended any attempt to tie the dollar to gold) by using a polynomial with several terms:

[tex] \[\mathrm{p}\left( t\right) =c\,{t}^{2}+b\,t+a\] [/tex]

Where [tex]\mathrm{p}\left( t\right)[/tex] is the gold price as a function of the time [tex]t[/tex]. This is a simple mathematical model with little real-world justification. It will, in fact, make grossly unrealistic predictions that should call it into question. A polynomial model of the time series of real gold prices is:

[tex] \[\mathrm{p}\left( t\right) =l\,{t}^{11}+k\,{t}^{10}+j\,{t}^{9}+i\,{t}^{8}+h\,{t}^{7}\][/tex]

[tex]\[ + g\,{t}^{6}+f\,{t}^{5}+e\,{t}^{4}+d\,{t}^{3}+c\,{t}^{2}+b\,t+a\][/tex]

Polynomial Model of Gold Price (12 Terms)

One can approximate any continuous function as accurately as one would like with a sum of a series of powers. The problem is that a power such as [tex] t^{12} [/tex] will grow without bound as the independent variable [tex] t [/tex] grows. This is usually quite unrealistic. This is a simple illustration of the difference between a symbolic mathematical model of reality and our common sense every day sense of reality.

Apocalypse or Gold Bubble?

Many other mathematical models are possible. In fact, there are an infinite number of functions or curves that agree with the data during the period from 1970 to 2009. In this way, one can predict anything. In mathematical models of physical phenomenon, it is common to try to construct the model from a set of building block functions, or more generally terms such as terms in a differential equation. This may be arbitrary or justified by arguing that the building blocks represent fundamental building blocks of the physical process in some way. In practice, one is trying to capture regularities in the data that may recur in new data. For example, the position of a pendulum is periodic; it repeats over and over again. Simple harmonic motion of this type was one of the first kinds of behavior understood mathematically by the ancients. One can construct models of the gold price data that agree with the data quite well by eye using a collection of peaks rather than periodic functions. One might, for example, represent the seeming peaks in the gold price data as the Gaussian or Normal function, commonly referred to as the “Bell Curve,”

[tex]\[ N(t, \mu, \sigma) = \frac{1.0}{\sqrt{2\pi}\,\sigma} {{e}^{-\frac{1.0\,{\left( t-\mu\right) }^{2}}{{\sigma}^{2}}} }\][/tex]

A very simple model is the sum of two Gaussians:

[tex] \[\mathrm{p}\left( t\right) = A_1N(t,\mu_1,\sigma_1) + A_2 N(t, \mu_2, \sigma_2) \] [/tex]

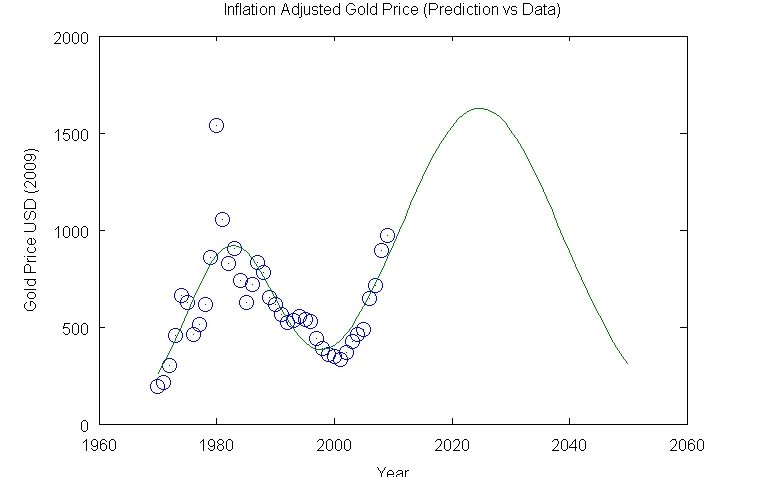

Gold 2 Gaussian Model

This simple model with two Gaussians does not agree very well with the data. It predicts the following future performance:

Gold 2 Gaussian Prediction

It predicts that the real price of gold will peak in about 2025 and then drop. One can get much better agreement between the model and the gold price data by adding more Gaussians, loosely corresponding to the apparent gold peaks in about 1974, 1982, 1987, 1993, and today. The spike in 1982 is especially sharp and can better be approximated by combining two Gaussians.

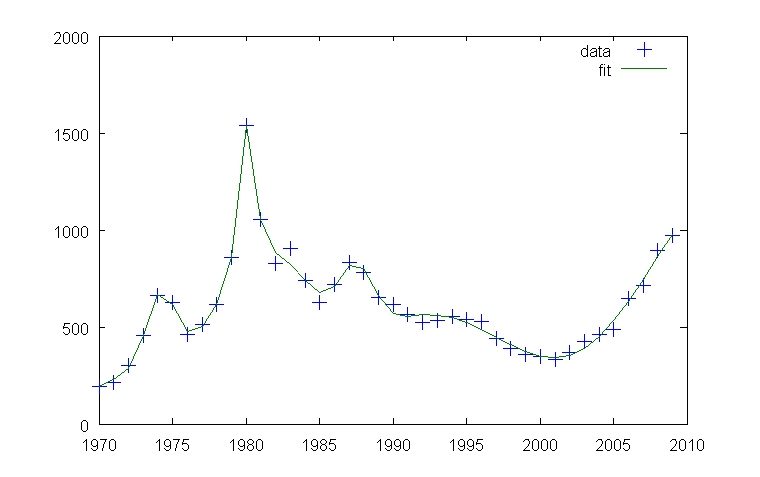

Gold 7 Gaussian Model

Now the agreement by eye is much better. The curves appear essentially the same. This model makes a different prediction.

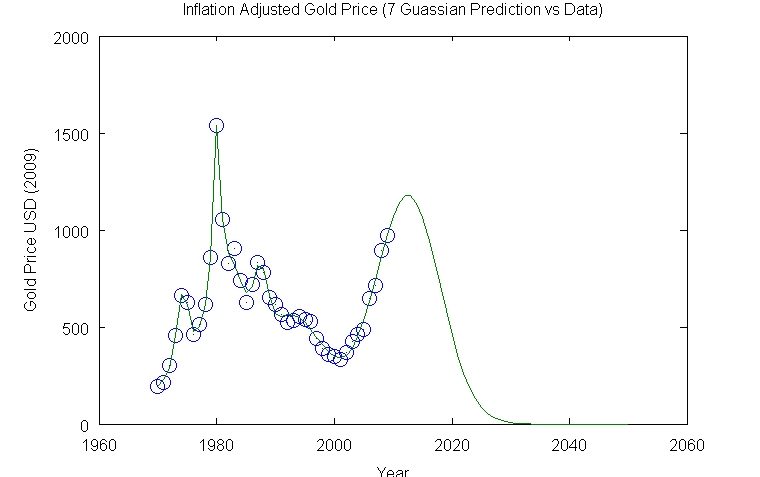

Gold 7 Gaussian Prediction

This model predicts a peak in real gold prices in just a few years, about 2012, followed by a decline to essentially zero. One can get significantly different predictions simply by using a different function to model the peaks in the gold price. For example, one can use the Cauchy-Lorentz distribution as a model for the peaks:

[tex]\[\mathrm{C}\left( t,\mu,\sigma\right) =\frac{1}{\frac{{\left( x-\mu\right) }^{2}}{{\sigma}^{2}}+1}\][/tex]

where [tex]t[/tex] is the time (year in this case), [tex] \mu [/tex] is the location of the peak, and [tex] \sigma [/tex] is a measure of the width or dispersion of the peak. Initially, one can try a model with two peaks:

[tex] \[\mathrm{p}\left( t\right) = A_1C(t,\mu_1,\sigma_1) + A_2 C(t, \mu_2, \sigma_2) \] [/tex]

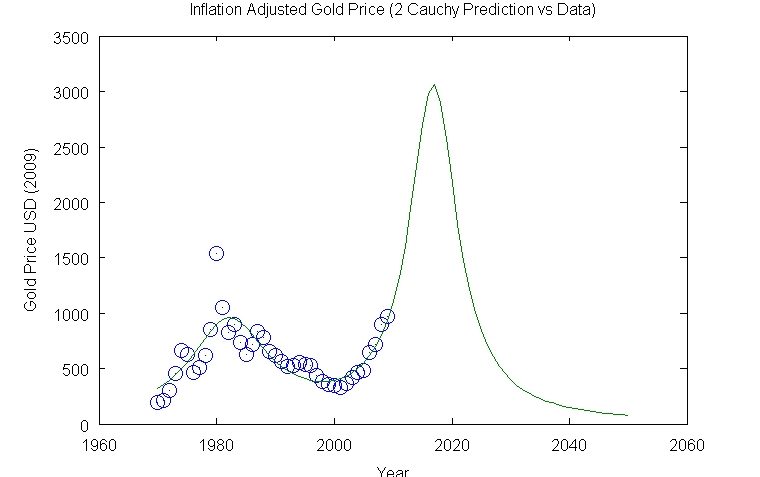

Gold 2 Cauchy Model

This model looks very similar to the two Gaussian model. It predicts something different however.

Gold 2 Cauchy Prediction

In this case, the price of gold trails off slowly instead of dropping to essentially zero in about a decade. This is a difference between the Gaussian and the Cauchy-Lorentz functions. Of course, the agreement between the model and data is not very good. One probably would not and should not trust it. One can achieve better agreement with more peaks, just as in the Gaussian models.

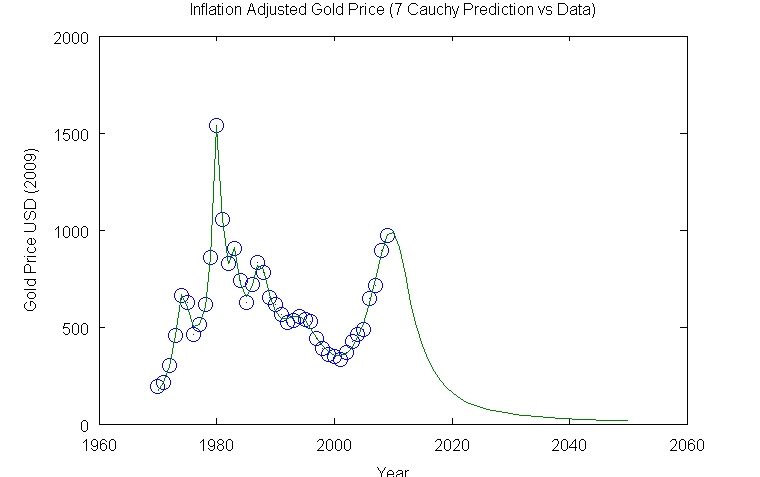

Gold 7 Cauchy Model

Now the agreement is almost exact by eye. The prediction however differs from the seven Gaussian model.

Gold 7 Cauchy Prediction

Again, the price of gold trails off slowly over a period of decades due to the difference between the Gaussian and Cauchy-Lorentz peak models. In fact, one can get essentially any prediction by choosing the appropriate mathematical model. How reasonable are these predictions? There are several theories about the present rise in gold prices. One clear contender is that the gold price rise in the last decade is yet another speculative financial bubble. In this scenario, one would expect the price of gold to drop substantially within a decade. One might also argue that the sharp run-up in gold prices will encourage overproduction of gold and the development of better gold refining, recycling technologies, alternatives to gold, and even perhaps the alchemist’s dream of converting base metals into gold (using nuclear reactors for example). At the other extreme, the rise in gold prices is tied to apocalyptic scenarios in which the US and other governments go bankrupt due to deficit spending and the dollar and other paper currencies becomes as valueless as the German mark during the infamous German hyperinflation. Thus, the real inflation-adjusted price of gold spikes as investors seek an inflation proof haven. Unfortunately, civilization collapses. Gold and other luxury items become valueless in the bitter Darwinian battle for survival in the post-apocalyptic world. The most valuable possessions are a gun, ammunition, and a large horde of dried food — all purchased from advertisers on Alex Jones web site. In either scenario, gold eventually tanks.

All kidding aside, it is usually possible to find technically sophisticated, plausible justifications for mathematical models. Usually does not mean always. The behavior of the polynomial models is grossly unrealistic. How likely is it that the price of gold would go negative, let alone extremely negative — meaning that people would be paying large sums of money to get rid of gold? The evidence that the Earth is nearly spherical with a diameter of about 8000 miles is very strong. Any argument that the Earth is really flat is extremely difficult to make in the present day. Most of us are pretty confident that the Sun will set today and rise again tomorrow and continue to do so for many, many years to come. There is some knowledge that is pretty certain. There are some mathematical models that have proven extremely accurate and reliable.

Nonetheless, it is usually possible to find plausible arguments for mathematical models and conceptual theories. One can usually explain away even grossly contradictory — “falsifying” in the language of Karl Popper — observations or experiments in a technically sophisticated, plausible way. This can create the illusion that a theory or mathematical model falls into the category of almost certain knowledge, our common sense notion of a fact. Once upon a time, many people believed that it was a fact that the Earth was flat. How could it possibly be a sphere? Political power, social status, and sizable funding tend to flow to those who claim certainty, to know hard facts rather than speculative theories. In common thinking, an expert is someone who says “I know the answer.” not someone who says “I don’t know.”

Scientists and science popularizers often seek to promote reigning scientific theories to the level of “almost certain” knowledge or “facts,” such as that the Earth is roughly spherical or the historical fact of the Holocaust. These latter two are the most common analogies cited in the popular science literature. Scientific theories are said to be supported by “overwhelming evidence.” There is a “consensus” that the theory is correct. The theory is no longer a theory, but a fact. In debates about evolution and creation, one encounters the curious claim that evolution is a falsifiable theory, that creationism or “intelligent design” is not falsifiable and thus not scientific, and that evolution is also a fact beyond any reasonable dispute or falsification. Increasingly, malcontents or die-hards who question the “consensus” are “deniers” or “denialists” in analogy to Holocaust deniers, an extremely emotional analogy indeed. There are now evolution deniers, AIDS deniers, global warming deniers, and a growing list of other deniers. Yet, certain knowledge is relatively rare especially in the frontiers of science.

In the case of gold, one can make a strong argument that the models above are unlikely to be correct. There is a certain fundamental demand for gold for industrial uses, in electronics for example. There is a long history of people buying gold for jewelry. The economic and political problems, the fears and the greed, that have historically driven the fluctuations in the price of gold are likely to continue through the 21st century. Thus, one should doubt models that show the real price of gold dropping to zero or nearly zero. Yet, both symbolic mathematics and verbal reasoning enable one to make a plausible argument that this will happen, supported by fancy symbolic mathematics and technical graphs.

A Deep Problem

It is always possible to perfectly match or fit any set of [tex]N[/tex] data points using a linear combination of at least [tex]N[/tex] linearly independent functions. Under many conditions, a function or composition of building block functions with [tex]N[/tex] adjustable parameters can also match or fit any set of [tex]N[/tex] data points. In addition, with creativity and trial and error, one can often construct mathematical models with less than [tex]N[/tex] parameters or building block functions that nonetheless do a good job of matching or fitting [tex]N[/tex] data points. These models may often fail to predict future data or data that lies outside of the region used to make the model or fit.

In general, a composition of a set of building block functions has a sort of plasticity, a certain ability to match any data to some degree. If there are [tex]N[/tex] building block functions or adjustable parameters and [tex]N[/tex] data points, this plasticity can be rigorously shown to be essentially infinite, that is the model can always match any set of [tex]N[/tex] data points. The philosopher of science Karl Popper called such models or theories unfalsifiable. They can never be proven wrong. They predict everything and therefore they also predict nothing. Unlike popular presentations of his doctrine of falsifiability, Popper recognized that falsifiability was often not a black and white distinction. There were degrees of falsifiability and he tried to define some logical and quantitative criterion for the degree of falsifiability. What this means is that a mathematical model or theory with [tex]M[/tex] adjustable parameters where [tex]M[/tex] is less than the number of data points [tex]N[/tex] may still match a broad class of possible observations or data. It can be falsified, perhaps, but only with great difficulty. There is, in the examples above, a lot of freedom to match many different sets of data with seven peaks in the model. The models have 21 adjustable parameters and there are 40 data points (40 years). Although the models cannot exactly match all sets of 40 data points, nonetheless they are likely to be good enough for most purposes. Remaining differences between the data and the models can easily be attributed to noise, measurement errors, or some similar excuse.

In physics, there are some examples of very large data sets that match very simple mathematical formulas. The motions of the planets in the Solar System conform to Kepler’s Laws and Newton’s theory of gravitation to a very high degree. This is not necessarily true for the motion of stars in the Milky Way galaxy, galaxies in galactic clusters and so forth. A deviation from Newtonian gravity is a possible explanation for the anomalies often cited as evidence for so-called “dark matter” or “dark energy.” So too, there is an enormous amount of quantitative data on the vibration of springs and strings, the motion of pendulums, simple radioactive decays, and various other physical phenomena that show precise matches to simple mathematical expressions such as Hooke’s Law for springs or exponential decay for radioactive decay. It is fair to say that the amount of data points is now in the millions or more and the models have only a few adjustable parameters such as the half-life of a radioactive isotope. Consequently, it is probably reasonable to have a high degree of confidence in these models. At the other extreme, it is clear that we should put no confidence in the predictive power of models with as many adjustable parameters or building block functions as the number of data points.

In many situations however including the frontiers of human knowledge and often areas like economics, the situation falls into a gray area. The theories, both symbolic mathematical models and conceptual models, may be complex, but not so complex as to be obviously “unfalsifiable.” The amount of data may be limited or of questionable quality, but still not obviously inadequate to draw conclusions. It is here that faulty human judgment is in practice applied, in part because human judgment, fallible though it undoubtedly is, is still the best option, more reliable than symbolic mathematics or computer programs in many cases. In constructing mathematical models in these cases, human judgment is often hidden in the definition of the symbols and the choice of building block functions or other mathematical components used in the model.

Economics, finance, politics and other human activities are especially treacherous areas for mathematical modeling. The mathematical and scientific methods used in physics and other “hard” sciences were developed to study highly repeatable phenomena that do not appear to change appreciably over time. For example, a “fair” coin will come up heads when flipped on average half the time, tails half the time. This was true in the early days of probability and statistics during the Renaissance. It is true today. Fair games of chance work the same way today as yesterday, last year, last century, and presumably thousands of years ago or in the future. One can collect vast amounts of data on these games. Similarly, physical phenomena such as the motion of the planets, radioactive decay, and so forth appear to behave the same way time after time. They do not evolve, learn from mistakes, forget lessons learned, or suddenly change for difficult to understand reasons. None of this is true of much economic or financial data.

In the example of gold, the behavior of gold changed radically from 1968 to August 1971 when the gold standard ended. Since 1970, there have been extensive political, economic, and technological changes that probably effect the price of gold. The Cold War ended. Apartheid in gold producing South Africa ended, followed by a large exodus of the white minority who dominated the mining industry. The use of electronics has increased; gold is used in electronics. Women’s fashions in clothing and jewelry have changed. The terrorist attacks of September 11, 2001 probably contributed to general unease and the rise in gold prices. Against these many changes, there is only forty years of data on gold prices. Day to day gold prices are correlated and gold seems to follow trends over several years, seemingly rising and falling in peaks. Thus, there is very limited data to analyze compared to a physical process. At the same time, one still has the freedom to construct many different mathematical models, theoretically an infinite number.

This ability to construct many different models that agree with observations or experiment but which make quite different predictions is not a problem unique to symbolic mathematical models. Rather, we encounter the same or a similar problem in everyday life, in politics, in personal relationships, where concepts, words, and pictures are the norm rather than symbolic mathematics with its illusion of certainty. It occurs when opposing attorneys are able to present radically different interpretations of the same evidence in a court case. It occurs when political activists explain the same events in radically different ways that almost always confirm their beliefs. It occurs in disputes between co-workers where each sees the same event or problem quite differently (it is all your fault). It occurs in conflicts between husbands and wives when each sees the same events differently. If verbal concepts and mental pictures are actually mathematical models maintained in the brain (but not in a symbolic way), then it may well be exactly the same problem as that encountered in mathematical modeling.

There is no doubt that human judgment is faulty and limited. In some relatively rare cases mathematics or formal logic can clearly outperform human judgment. Nonetheless, in many situations, human judgment and intuition still win out over mathematics, formal logic, or computer programs. It remains an unsolved and perhaps unsolvable problem to find a way to select the right model that, in fact, predicts new observations as well or even better than human judgment.

The nature and origin of human judgment and intuition remains an enigma. Governments have spent billions of dollars and decades on artificial intelligence in the mostly futile effort to replicate even sometimes seemingly simple aspects of human reasoning. Human beings often cannot explain either verbally or in symbolic logical or mathematical ways their successful reasoning processes. Ancient scholars and philosophers might attribute their ideas to divine inspiration or mystical insight. Indeed historical accounts of inventions and discoveries are replete with reported sudden insights or realizations such as the famous story of Archimedes in his bathtub suddenly realizing how to determine the gold content of the King’s crown without destroying the crown and then racing naked through the streets of Syracuse shouting “Heureka!” One may wonder what Archimedes feared the King would do to him if he had failed to solve the problem. The modern scientific view would probably attribute this ability of the human mind to find the right answer to an anthropic or evolutionary cause. Our brain incorporates billions of years of evolution and is thus tuned to the mysterious underlying logical or mathematical structure of the universe.

Conclusion

It is important to realize that one can construct an infinite number of mathematical models that match a set of data. In some sense, one can construct an even “larger” number of mathematical models that match a set of data “well enough,” where remaining differences can easily be attributed to noise, instrument error, or minor effects that can be ignored for practical purposes. In high school and college, one is often exposed to mathematics and geometry as a rigorous deductive system. The epitome of this is Euclid’s geometry which many people are exposed to in high school; high school math courses typically teach the first three of Euclid’s thirteen books. One starts with axioms and definitions that often seem self-evident, with the possible exception of the so-called parallel postulate. One can apply a sequence of logical steps to get a precise unambiguous answer. Similarly, high school and college science courses frequently focus primarily on extremely well-measured phenomena such as vibrating springs or radioactive decay that precisely follow simple mathematical laws. Scientists are often described as “deriving,” “figuring out,” or “deducing” mathematical laws such as Newton’s Theory of Gravitation, Maxwell’s Equations of Electromagnetism, or Schrodinger’s Equation for quantum mechanics. The implication is that these mathematical theories can be found by the application of rigorous mathematical or logical rules, much in the way that theorems in Euclidean geometry are proven. This has a great appeal compared to messy, fallible human judgment and intuition. But the reality is that the theories were found through the application of messy, fallible human judgment and intuition, perhaps assisted by some mathematics, by model fitting methods, and so forth, but in the end it was mysterious human judgment and intuition.

If we could understand what human beings are actually doing, this would be a great advance. It would be an even greater advance to find a way to improve human judgment and intuition, which is certainly quite fallible.

In the meantime, it is particularly hazardous to try to apply mathematical modeling to economics, finance, and human behavior. This does not mean that we should not try. Nor does it mean that there may not be successes in applying mathematics to human activity. Indeed, in economics, there are some mathematical rules of thumb that are often correct. It is, for example, generally observed that inflation is lower when unemployment is higher; this relation loosely follows a mathematical curve. However, we are a very long distance from a predictive mathematical method comparable to Isaac Asimov’s fictional psychohistory if this is even possible. Most people don’t think in mathematics; can human behavior really be reduced to mathematics?

The present financial crisis illustrates that these seemingly abstruse issues of mathematical models can impact the lives of many people and organizations. This is, if anything, likely to increase with growing reliance on computers and mathematical models implemented in computer software and hardware. There remains no greater wisdom than the ancient Latin saying: Caveat Emptor (Buyer Beware).

Note: An appendix with the technical details of the analysis and plots presented above follows the Suggested Reading/References section below. This includes the raw data, the models, and the Octave scripts used to fit the models to the annual gold price data. This article is primarily for informational and educational purposes. It is not investment advice.

Copyright © 2010 John F. McGowan, Ph.D.

About the Author

John F. McGowan, Ph.D. is a software developer, research scientist, and consultant. He works primarily in the area of complex algorithms that embody advanced mathematical and logical concepts, including speech recognition and video compression technologies. He has extensive experience developing software in C, C++, Visual Basic, Mathematica, MATLAB, and many other programming languages. He is probably best known for his AVI Overview, an Internet FAQ (Frequently Asked Questions) on the Microsoft AVI (Audio Video Interleave) file format. He has worked as a contractor at NASA Ames Research Center involved in the research and development of image and video processing algorithms and technology. He has published articles on the origin and evolution of life, the exploration of Mars (anticipating the discovery of methane on Mars), and cheap access to space. He has a Ph.D. in physics from the University of Illinois at Urbana-Champaign and a B.S. in physics from the California Institute of Technology (Caltech). He can be reached at jmcgowan11@earthlink.net.

Suggested Reading/References

Karl Popper, The Logic of Scientific Discovery, Routledge, London, England 2000 (First published 1959, English translation with new notes and appendices of Logik der Forschung, published Vienna, Austria, 1934)

Paul Feyerabend, Against Method (3rd Edition), Verso, 1993

Thomas Kuhn, The Structure of Scientific Revolutions, University Of Chicago Press; 3rd edition (December 15, 1996)

John D. Barrow and Frank J. Tipler, The Anthropic Cosmological Principle, Oxford University Press, New York, 1986

Isaac Asimov, Foundation, Spectra; Revised edition (October 1, 1991)

Roger Lowenstein, When Genius Failed: The Rise and Fall of Long Term Capital Management, Random House, New York, 2000

Emanuel Derman, My Life as a Quant: Reflections on Physics and Finance, John Wiley and Sons, Hoboken, New Jersey, 2004

Charles MacKay, Extraordinary Popular Delusions and the Madness of Crowds, Farrar, Straus, and Giroux, New York, 1932 (first published in London in 1841)

Robert J. Shiller, Irrational Exuberance, Broadway Books, New York, 2000

Dean Baker, False Profits: Recovering from the Bubble Economy, Polipoint Press (January 15, 2010)

Michael Specter, Denialism: how irrational thinking hinders scientific progress, harms the planet, and threatens our lives, Penguin Press, 2009

Seth C. Kalichman, Denying AIDS: Conspiracy Theories, Pseudoscience, and Human Tragedy, Springer, 2009

Bill McKibben, “Hot Mess: Why are conservatives so radical about climate?”, The New Republic, October 6, 2010

Appendix: Technical Details

The annual gold price data used in this article is from the World Gold Council. Here is the actual raw data.

1900 20.67 4.25 o 1900 8.14 0.037941643 544.78 1913-01-01 0.10 1901 20.67 4.25 o 1901 8.24 0.038407756 538.17 1913-01-02 0.10 1902 20.67 4.25 o 1902 8.34 0.03887387 531.72 1913-01-03 0.10 1903 20.67 4.25 o 1903 8.53 0.039759485 519.88 1913-01-04 0.10 1904 20.67 4.25 o 1904 8.63 0.040225599 513.85 1913-01-05 0.10 1905 20.67 4.25 o 1905 8.53 0.039759485 519.88 1913-01-06 0.10 1906 20.67 4.25 o 1906 8.72 0.040645101 508.55 1913-01-07 0.10 1907 20.67 4.25 o 1907 9.11 0.042462944 486.78 1913-01-08 0.10 1908 20.67 4.25 o 1908 8.92 0.041577328 497.15 1913-01-09 0.10 1909 20.67 4.25 o 1909 8.82 0.041111215 502.78 1913-01-10 0.10 1910 20.67 4.25 o 1910 9.21 0.042929058 481.49 1913-01-11 0.10 1911 20.67 4.25 o 1911 9.21 0.042929058 481.49 1913-01-12 0.10 1912 20.67 4.25 o 1912 9.4 0.043814673 471.76 1914-01-01 0.10 1913 20.67 4.25 12/31/1913 1913 9.6 0.04630723 446.37 10 1914-01-02 0.10 1914 20.67 4.25 12/31/1914 1914 9.69 0.046770302 441.95 10.1 1914-01-03 0.10 1915 20.67 4.25 12/31/1915 1915 9.74 0.047696447 433.37 10.3 1914-01-04 0.10 1916 20.67 4.25 12/31/1916 1916 10.64 0.053716387 384.80 11.6 1914-01-05 0.10 1917 20.67 4.25 12/31/1917 1917 12.82 0.063440905 325.82 13.7 1914-01-06 0.10 1918 20.67 4.25 12/31/1918 1918 15.06 0.076406929 270.53 16.5 1914-01-07 0.10 1919 20.67 4.50 12/31/1919 1919 17.3 0.087520665 236.17 18.9 1914-01-08 0.10 1920 20.67 5.60 12/31/1920 1920 20.04 0.089836026 230.09 19.4 1914-01-09 0.10 1921 20.67 5.35 12/31/1921 1921 17.9 0.080111508 258.02 17.3 1914-01-10 0.10 1922 20.67 4.69 12/31/1922 1922 16.77 0.078259219 264.12 16.9 1914-01-11 0.10 1923 20.67 4.51 12/31/1923 1923 17.07 0.080111508 258.02 17.3 1914-01-12 0.10 1924 20.67 4.68 12/31/1924 1924 17.1 0.080111508 258.02 17.3 1915-01-01 0.10 1925 20.67 4.25 12/31/1925 1925 17.53 0.082889942 249.37 17.9 1915-01-02 0.10 1926 20.67 4.25 12/31/1926 1926 17.7 0.081963797 252.18 17.7 1915-01-03 0.10 1927 20.67 4.25 12/31/1927 1927 17.37 0.080111508 258.02 17.3 1915-01-04 0.10 1928 20.67 4.25 12/31/1928 1928 17.13 0.079185363 261.03 17.1 1915-01-05 0.10 1929 20.67 4.25 12/31/1929 1929 17.13 0.079648436 259.52 17.2 1915-01-06 0.10 1930 20.67 4.25 12/31/1930 1930 16.7 0.07455464 277.25 16.1 1915-01-07 0.10 1931 20.67 4.25 12/31/1931 1931 15.23 0.067608556 305.73 14.6 1915-01-08 0.10 1932 20.67 5.90 12/31/1932 1932 13.66 0.060662471 340.74 13.1 1915-01-09 0.10 1933 20.67 6.24 12/31/1933 1933 12.96 0.061125544 338.16 13.2 1915-01-10 0.10 1934 35.00 6.88 12/31/1934 1934 13.39 0.062051688 564.05 13.4 1915-01-11 0.10 1935 35.00 7.11 12/31/1935 1935 13.73 0.063903977 547.70 13.8 1915-01-12 0.10 1936 35.00 7.02 12/31/1936 1936 13.86 0.064830122 539.87 14 1916-01-01 0.10 1937 35.00 7.04 12/31/1937 1937 14.36 0.066682411 524.88 14.4 1916-01-02 0.10 1938 35.00 7.13 12/31/1938 1938 14.09 0.064830122 539.87 14 1916-01-03 0.11 1939 35.00 7.72 12/31/1939 1939 13.89 0.064830122 539.87 14 1916-01-04 0.11 1940 35.00 8.40 12/31/1940 1940 14.03 0.065293194 536.04 14.1 1916-01-05 0.11 1941 35.00 8.40 12/31/1941 1941 14.73 0.071776206 487.63 15.5 1916-01-06 0.11 1942 35.00 8.40 12/31/1942 1942 16.3 0.078259219 447.23 16.9 1916-01-07 0.11 1943 35.00 8.40 12/31/1943 1943 17.3 0.08057458 434.38 17.4 1916-01-08 0.11 1944 35.00 8.40 12/31/1944 1944 17.6 0.082426869 424.62 17.8 1916-01-09 0.11 1945 35.00 8.61 12/31/1945 1945 18 0.084279159 415.29 18.2 1916-01-10 0.11 1946 35.00 8.61 12/31/1946 1946 19.54 0.099560544 351.54 21.5 1916-01-11 0.12 1947 35.00 8.61 12/31/1947 1947 22.34 0.108358918 323.00 23.4 1916-01-12 0.12 1948 35.00 8.68 12/31/1948 1948 24.08 0.111600424 313.62 24.1 1917-01-01 0.12 1949 35.00 9.40 12/31/1949 1949 23.85 0.109285063 320.26 23.6 1917-01-02 0.12 1950 35.00 12.50 12/31/1950 1950 24.08 0.115768075 302.33 25 1917-01-03 0.12 1951 35.00 12.50 12/31/1951 1951 25.98 0.122714159 285.22 26.5 1917-01-04 0.13 1952 35.00 12.50 12/31/1952 1952 26.55 0.123640304 283.08 26.7 1917-01-05 0.13 1953 35.00 12.50 12/31/1953 1953 26.75 0.124566449 280.97 26.9 1917-01-06 0.13 1954 35.00 12.50 12/31/1954 1954 26.88 0.123640304 283.08 26.7 1917-01-07 0.13 1955 35.00 12.50 12/31/1955 1955 26.78 0.124103376 282.02 26.8 1917-01-08 0.13 1956 35.00 12.50 12/31/1956 1956 27.18 0.127807955 273.85 27.6 1917-01-09 0.13 1957 35.00 12.50 12/31/1957 1957 28.15 0.131512533 266.13 28.4 1917-01-10 0.14 1958 35.00 12.50 12/31/1958 1958 28.92 0.133827895 261.53 28.9 1917-01-11 0.14 1959 35.00 12.50 12/31/1959 1959 29.16 0.136143256 257.08 29.4 1917-01-12 0.14 1960 35.00 12.50 12/31/1960 1960 29.62 0.137995545 253.63 29.8 1918-01-01 0.14 1961 35.00 12.50 12/31/1961 1961 29.92 0.13892169 251.94 30 1918-01-02 0.14 1962 35.00 12.50 12/31/1962 1962 30.26 0.140773979 248.63 30.4 1918-01-03 0.14 1963 35.00 12.50 12/31/1963 1963 30.62 0.143089341 244.60 30.9 1918-01-04 0.14 1964 35.00 12.50 12/31/1964 1964 31.03 0.144478557 242.25 31.2 1918-01-05 0.15 1965 35.00 12.50 12/31/1965 1965 31.56 0.147256991 237.68 31.8 1918-01-06 0.15 1966 35.00 12.50 12/31/1966 1966 32.46 0.152350787 229.73 32.9 1918-01-07 0.15 1967 35.00 12.65 12/31/1967 1967 33.4 0.15698151 222.96 33.9 1918-01-08 0.15 1968 38.94 16.23 12/31/1968 1968 34.8 0.164390666 236.87 35.5 1918-01-09 0.16 1969 40.76 16.98 12/31/1969 1969 36.67 0.174578257 233.48 37.7 1918-01-10 0.16 1970 36.07 15.03 12/31/1970 1970 38.84 0.184302775 195.71 39.8 1918-01-11 0.16 1971 41.17 16.91 12/31/1971 1971 40.51 0.190322715 216.32 41.1 1918-01-12 0.17 1972 59.00 23.58 12/31/1972 1972 41.85 0.196805727 299.79 42.5 1919-01-01 0.17 1973 97.84 39.90 12/31/1973 1973 44.45 0.213939402 457.33 46.2 1919-01-02 0.16 1974 158.96 67.96 12/31/1974 1974 49.33 0.240334523 661.41 51.9 1919-01-03 0.16 1975 160.91 72.42 12/31/1975 1975 53.84 0.257005126 626.10 55.5 1919-01-04 0.17 1976 124.71 69.05 12/31/1976 1976 56.94 0.269508078 462.73 58.2 1919-01-05 0.17 1977 147.78 84.66 12/31/1977 1977 60.61 0.287567898 513.90 62.1 1919-01-06 0.17 1978 193.39 100.75 12/31/1978 1978 65.22 0.313499947 616.87 67.7 1919-01-07 0.17 1979 304.83 143.68 12/31/1979 1979 72.57 0.355176454 858.25 76.7 1919-01-08 0.18 1980 614.61 264.20 12/31/1980 1980 82.38 0.399631394 1537.94 86.3 1919-01-09 0.18 1981 459.26 226.47 12/31/1981 1981 90.93 0.435287962 1055.07 94 1919-01-10 0.18 1982 375.28 214.38 12/31/1982 1982 96.5 0.451958564 830.34 97.6 1919-01-11 0.19 1983 423.61 279.24 12/31/1983 1983 99.6 0.469092239 903.04 101.3 1919-01-12 0.19 1984 360.50 269.77 12/31/1984 1984 103.9 0.487615131 739.31 105.3 1920-01-01 0.19 1985 317.18 244.68 12/31/1985 1985 107.6 0.506138023 626.67 109.3 1920-01-02 0.20 1986 367.72 250.66 12/31/1986 1986 109.6 0.511694891 718.63 110.5 1920-01-03 0.20 1987 446.28 272.30 12/31/1987 1987 113.6 0.534385434 835.13 115.4 1920-01-04 0.20 1988 436.79 245.20 12/31/1988 1988 118.3 0.558002121 782.77 120.5 1920-01-05 0.21 1989 380.74 232.20 12/31/1989 1989 124 0.58393417 652.03 126.1 1920-01-06 0.21 1990 383.32 214.78 12/31/1990 1990 130.7 0.619590737 618.67 133.8 1920-01-07 0.21 1991 362.10 204.65 12/31/1991 1991 136.2 0.638576701 567.04 137.9 1920-01-08 0.20 1992 343.86 194.76 12/31/1992 1992 140.3 0.657099593 523.30 141.9 1920-01-09 0.20 1993 360.00 239.68 12/31/1993 1993 144.5 0.675159413 533.21 145.8 1920-01-10 0.20 1994 384.12 250.79 12/31/1994 1994 148.2 0.693219232 554.11 149.7 1920-01-11 0.20 1995 384.05 243.31 12/31/1995 1995 152.4 0.71081598 540.29 153.5 1920-01-12 0.19 1996 387.82 248.33 12/31/1996 1996 156.9 0.734432667 528.05 158.6 1921-01-01 0.19 1997 330.98 202.10 12/31/1997 1997 160.5 0.746935619 443.12 161.3 1921-01-02 0.18 1998 294.12 177.56 12/31/1998 1998 163 0.758975499 387.52 163.9 1921-01-03 0.18 1999 278.55 172.13 12/31/1999 1999 166.6 0.77935068 357.41 168.3 1921-01-04 0.18 2000 279.10 184.09 12/31/2000 2000 172.2 0.805745801 346.39 174 1921-01-05 0.18 2001 272.67 189.36 12/31/2001 2001 177.1 0.818248753 333.24 176.7 1921-01-06 0.18 2002 309.66 206.27 12/31/2002 2002 179.9 0.83769779 369.66 180.9 1921-01-07 0.18 2003 362.91 222.20 12/31/2003 2003 184 0.853442248 425.23 184.3 1921-01-08 0.18 2004 409.17 223.36 12/31/2004 2004 188.9 0.881226586 464.32 190.3 1921-01-09 0.18 2005 444.47 244.86 12/31/2005 2005 195.3 0.911326285 487.72 196.8 1921-01-10 0.18 2006 603.95 327.68 12/31/2006 2006 201.6 0.9344799 646.30 201.8 1921-01-11 0.17 2007 695.39 347.00 12/31/2007 2007 207.34 0.972618535 714.96 210.036 1921-01-12 0.17 2008 871.65 473.17 12/31/2008 2008 215.3 0.973507634 895.37 210.228 1922-01-01 0.17 2009 972.90 621.59 12/31/2009 2009 214.54 1 972.90 215.949 1922-01-02 0.17

The models were fitted to the data using the free Octave numerical programming environment. Octave is Matlab compatible and available under the GNU Public License. Octave is available in binary as well as source code versions for Windows, Mac OS, and Linux. The standard polyfit polynomial fitting function in Octave was used to fit the polynomial models to the annual gold price data. The leasqr least squares fitting function from the optim Octave add-on package was used to fit the Gaussian and Cauchy-Lorentz peak models to the annual gold price data. Octave Forge add-on packages are available as Unix style blatz.tar.gz files. There is no need to extract the contents of these files. Octave has a command pkg install which handles installing the packages; just type pkg install blatz.tar.gz. The GNU Octave installation includes a C/C++ compiler to compile any C or C++ files included in the package. Note that the run-time errors reported by Octave, for example due to a syntax error, can be cryptic. Be patient and don’t always trust the error message.

% plot_gold.m

% Description: Octave (Matlab compatible) script to plot annual gold price data

% and fit polynomial models to the data. Tested on Windows XP Service Pack 2

% with Octave 3.2.4 for Windows installed.

%

% Author: John F. McGowan, Ph.D.

% Copyright (C) 2010 by John F. McGowan

%

%

disp('reading gold price data...');

fflush(stdout);

data = dlmread('annual_gold_price_from_1900.txt');

disp('making plot 1');

fflush(stdout);

figure(1)

plot(data(:,1), data(:,8));

title('Inflation Adjusted Gold Price');

xlabel('Year');

ylabel('Gold Price USD (2009)');

disp('making plot 2');

fflush(stdout);

figure(2)

plot(data(:,1), data(:,2));

title('Nominal Gold Price');

xlabel('Year');

ylabel('Gold Price USD');

disp('making cpi plot');

figure(3)

plot(data(:,1), data(:,6));

title('US Consumer Price Index (CPI)');

xlabel('Year');

% annual inflation rate

disp('plotting annual inflation rate');

fflush(stdout);

figure(4)

cpi = data(:,6);

cpi_shift = shift(cpi,1);

inflation = (cpi - cpi_shift) ./ cpi_shift;

years = data(:,1);

plot(years(2:end), inflation(2:end)*100);

title('US Annual Inflation Rate');

xlabel('Year');

ylabel('Inflation (%)');

%

% fitting polynomial model to data 1970 to 2009

%

disp('making gold price prediction 12 terms');

fflush(stdout);

figure(5)

floating = years(71:end);

floating_gold_price = data(71:end, 8);

p = polyfit(floating, floating_gold_price, 12);

prediction = (1970:2020);

f = polyval(p, prediction);

plot(floating, floating_gold_price, 'o', prediction, f, '-');

title('Polynomial Model of Gold Price (12 Terms)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

disp('making gold price prediction 24 terms');

fflush(stdout);

figure(6)

floating = years(71:end);

floating_gold_price = data(71:end, 8);

p = polyfit(floating, floating_gold_price, 24);

prediction = (1970:2020);

f = polyval(p, prediction);

plot(floating, floating_gold_price, 'o', prediction, f, '-');

title('Polynomial Model of Gold Price (24 Terms)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

disp('making gold price prediction 32 terms');

fflush(stdout);

figure(7)

floating = years(71:end);

floating_gold_price = data(71:end, 8);

p = polyfit(floating, floating_gold_price, 32);

prediction = (1970:2020);

f = polyval(p, prediction);

plot(floating, floating_gold_price, 'o', prediction, f, '-');

title('Polynomial Model of Gold Price (32 Terms)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

disp('all done');

fflush(stdout);

% THE END

The script to fit the two Gaussian peak model to the data is:

% fit_gold.m

% Description: Octave (matlab compatible) script to fit two gaussian peak model

% to annual gold price data using Octave 3.2.4 and the optim package version 1.0.15

% Tested on Windows XP Service Pack 2 with Octave 3.2.4 and optim 1.0.15 installed.

%

% Author: John F. McGowan, Ph.D.

% Copyright (C) 2010 by John F. McGowan

%

disp('fitting model to gold price data');

fflush(stdout);

% fit model to gold price data

%floating_gold_price has inflation adjusted gold price since 1970

floating_years = years(71:end);

% Define functions

% model annual gold price data as two Gaussians

leasqrfunc = @(x,p) p(1) * exp(-1.0*(x - p(2)).^2/p(3)^2) + p(4) * exp(-1.0*(x - p(5)).^2/p(6)^2);

leasqrdfdp = @(x, f, p, dp, func) [exp(-1.0*(x - p(2)).^2/p(3)^2), (2*(x - p(2))/p(3)^2) * p(1) .* exp(-1.0*(x - p(2)).^2/p(3)^2), (2 * (x - p(2)).^2/p(3)^3) * p(1) .* exp(-1.0*(x - p(2)).^2/p(3)^2), exp(-1.0*(x - p(5)).^2/p(6)^2), (2*(x - p(5))/p(6).^2) * p(4) .* exp(-1.0*(x - p(5)).^2/p(6)^2), (2 * (x - p(5)).^2/p(6)^3) * p(4) .* exp(-1.0*(x - p(5)).^2/p(6)^2) ];

wt1 = ones(size(floating_gold_price));

t = floating_years;

data = floating_gold_price;

F = leasqrfunc;

dFdp = leasqrdfdp; % exact derivative

dp = [50.0; 1.0; 1.0; 50.0; 1.0; 1.0];

pin = [500.0; 1980.; 5.0; 500.0; 2010.0; 5.0 ];

stol=0.01; niter=50;

minstep = [10.0; 0.2; 0.2; 10.0; 0.2; 0.2];

maxstep = [100.0; 5.0; 5.0; 100.0; 5.0; 5.0];

options = [minstep, maxstep];

disp(size(t));

disp(size(data));

disp(size(wt1));

fflush(stdout);

figure(1);

global verbose;

verbose = 1;

[f1, p1, kvg1, iter1, corp1, covp1, covr1, stdresid1, Z1, r21] = ...

leasqr (t, data, pin, F, stol, niter, wt1, dp, dFdp, options);

%

% make a prediction

figure(2);

pred_years = [1970:2020];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

figure(3);

pred_years = [1970:2050];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

figure(4);

pred_years = [1970:2100];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

data_2G = data;

model_2G = leasqrfunc(floating_years, p1);

diff_2G = model_2G - data_2G;

chisq_2G = diff_2G' * diff_2G;

disp('all done');

% THE END

The script to fit the seven (7) Gaussian peak model to the annual gold price data is:

% fit_gold7.m

% Description: Octave (matlab compatible) script to fit seven (7) Gaussian peak model

% to annual gold price data.

% Tested using Octave 3.2.4 with optim 1.0.15 add on package installed on Windows XP Service Pack 2

% Author: John F. McGowan, Ph.D.

% Copyright (C) John F. McGowan

%

disp('fitting 7 Gaussian model to gold price data');

fflush(stdout);

% fit model to gold price data

%floating_gold_price has inflation adjusted gold price since 1970

floating_years = years(71:end);

% Define functions

% model as seven (7) un-normalized Gaussians

leasqrfunc = @(x,p) p(1) * exp(-1.0*(x - p(2)).^2/p(3)^2) + p(4) * exp(-1.0*(x - p(5)).^2/p(6)^2) + p(7) * exp(-1.0*(x - p(8)).^2/p(9)^2) + p(10) * exp(-1.0*(x - p(11)).^2/p(12)^2) + p(13) * exp(-1.0*(x - p(14)).^2/p(15)^2) + p(16) * exp(-1.0*(x - p(17)).^2/p(18)^2) + p(19) * exp(-1.0*(x - p(20)).^2/p(21)^2);

leasqrdfdp = @(x, f, p, dp, func) [exp(-1.0*(x - p(2)).^2/p(3)^2), (2*(x - p(2))/p(3)^2) * p(1) .* exp(-1.0*(x - p(2)).^2/p(3)^2), (2 * (x - p(2)).^2/p(3)^3) * p(1) .* exp(-1.0*(x - p(2)).^2/p(3)^2), exp(-1.0*(x - p(5)).^2/p(6)^2), (2*(x - p(5))/p(6).^2) * p(4) .* exp(-1.0*(x - p(5)).^2/p(6)^2), (2 * (x - p(5)).^2/p(6)^3) * p(4) .* exp(-1.0*(x - p(5)).^2/p(6)^2), exp(-1.0*(x - p(8)).^2/p(9)^2), (2*(x - p(8))/p(9)^2) * p(7) .* exp(-1.0*(x - p(8)).^2/p(9)^2), (2 * (x - p(8)).^2/p(9)^3) * p(7) .* exp(-1.0*(x - p(8)).^2/p(9)^2) , exp(-1.0*(x - p(11)).^2/p(12)^2), (2*(x - p(11))/p(12)^2) * p(10) .* exp(-1.0*(x - p(11)).^2/p(12)^2), (2 * (x - p(11)).^2/p(12)^3) * p(10) .* exp(-1.0*(x - p(11)).^2/p(12)^2) , exp(-1.0*(x - p(14)).^2/p(15)^2), (2*(x - p(14))/p(15)^2) * p(13) .* exp(-1.0*(x - p(14)).^2/p(15)^2), (2 * (x - p(14)).^2/p(15)^3) * p(13) .* exp(-1.0*(x - p(14)).^2/p(15)^2), exp(-1.0*(x - p(17)).^2/p(18)^2), (2*(x - p(17))/p(18)^2) * p(16) .* exp(-1.0*(x - p(17)).^2/p(18)^2), (2 * (x - p(17)).^2/p(18)^3) * p(16) .* exp(-1.0*(x - p(17)).^2/p(18)^2) , exp(-1.0*(x - p(20)).^2/p(21)^2), (2*(x - p(20))/p(21)^2) * p(19) .* exp(-1.0*(x - p(20)).^2/p(21)^2), (2 * (x - p(20)).^2/p(21)^3) * p(19) .* exp(-1.0*(x - p(20)).^2/p(21)^2) ];

wt1 = ones(size(floating_gold_price));

t = floating_years;

data = floating_gold_price;

F = leasqrfunc;

dFdp = leasqrdfdp; % exact derivative

dp = [50.0; 1.0; 1.0; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0 ; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0];

pin = [500.0; 1980.; 5.0; 500.0; 2010.0; 5.0; 500.0; 1982; 2.0; 500.0; 1987; 2.0; 500.0; 1995; 5.0 ; 500.0; 1974; 5.0; 500.0; 1974; 5.0 ];

stol=0.01; niter=100;

minstep = [10.0; 0.2; 0.2; 10.0; 0.2; 0.2; 10.0; 0.2; 0.2; 10.0; 0.1; 0.1; 10.0; 0.1; 0.1; 10.0; 0.1; 0.1; 10.0; 0.1; 0.1];

maxstep = [100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0];

options = [minstep, maxstep];

disp(size(t));

disp(size(data));

disp(size(wt1));

fflush(stdout);

figure(1);

global verbose;

verbose = 1;

[f1, p1, kvg1, iter1, corp1, covp1, covr1, stdresid1, Z1, r21] = ...

leasqr (t, data, pin, F, stol, niter, wt1, dp, dFdp, options);

%

% make a prediction

figure(2);

pred_years = [1970:2020];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (7 Gaussian Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

figure(3);

pred_years = [1970:2050];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (7 Guassian Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

figure(4);

pred_years = [1970:2100];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (7 Gaussian Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

data_7G = data;

model_7G = leasqrfunc(floating_years, p1);

diff_7G = model_7G - data_7G;

chisq_7G = diff_7G' * diff_7G;

disp('all done (7 Gaussian Fit) all done');

% THE END

The script to fit the two Cauchy-Lorentz function peak model to the annual gold price data is:

% fit_gold_cauchy.m

% Description: Octave (matlab compatible) script to fit a two Cauchy-Lorentz peak model to the annual gold price data. Tested using Octave 3.2.4 and the optim 1.015 add-on package on Windows XP Service Pack 2.

% Author: John F. McGowan, Ph.D.

% Copyright (C) John F. McGowan

%

disp('fitting 2 Cauchy-Lorentz model to gold price data');

fflush(stdout);

% fit model to gold price data

%floating_gold_price has inflation adjusted gold price since 1970

floating_years = years(71:end);

% Define functions

% model as the linear combination of two Cauchy-Lorentz (aka Breit-Wigner) functions

leasqrfunc = @(x,p) p(1) ./(1 + (x - p(2)).^2/p(3)^2) + p(4) ./(1 + (x - p(5)).^2/p(6)^2);

leasqrdfdp = @(x, f, p, dp, func) [1.0 ./(1.0 + (x - p(2)).^2/p(3)^2), (2*p(1)*(x-p(2)))./(p(3)^2*((x-p(2)).^2/p(3)^2+1).^2), (2*p(1)*(x-p(2)).^2)./(p(3)^3*((x-p(2)).^2/p(3)^2+1).^2), 1.0 ./(1.0 + (x - p(5)).^2/p(6)^2), (2*p(4)*(x-p(5)))./(p(6)^2*((x-p(5)).^2/p(6)^2+1).^2), (2*p(4)*(x-p(5)).^2)./(p(6)^3*((x-p(5)).^2/p(6)^2+1).^2)];

wt1 = ones(size(floating_gold_price));

t = floating_years;

data = floating_gold_price;

F = leasqrfunc;

dFdp = leasqrdfdp; % exact derivative

dp = [50.0; 1.0; 1.0; 50.0; 1.0; 1.0];

pin = [500.0; 1980.; 5.0; 500.0; 2010.0; 5.0 ];

stol=0.01; niter=50;

minstep = [10.0; 0.2; 0.2; 10.0; 0.2; 0.2];

maxstep = [100.0; 5.0; 5.0; 100.0; 5.0; 5.0];

options = [minstep, maxstep];

disp(size(t));

disp(size(data));

disp(size(wt1));

fflush(stdout);

figure(1);

global verbose;

verbose = 1;

[f1, p1, kvg1, iter1, corp1, covp1, covr1, stdresid1, Z1, r21] = ...

leasqr (t, data, pin, F, stol, niter, wt1, dp, dFdp, options);

%

% make a prediction

figure(2);

pred_years = [1970:2020];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (2 Cauchy Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

figure(3);

pred_years = [1970:2050];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (2 Cauchy Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

figure(4);

pred_years = [1970:2100];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (2 Cauchy Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

% C suffix for Cauchy Lorentz model

data_2C = data;

model_2C = leasqrfunc(floating_years, p1);

diff_2C = model_2C - data_2C;

chisq_2C = diff_2C' * diff_2C;

disp('all done');

% THE END

The Octave script to fit the seven (7) Cauchy-Lorentz peak model to the annual gold price data is:

% fit_gold7.m

% Description: Octave (matlab compatible) script to fit seven (7) Cauchy-Lorentz peak model

% to annual gold price data.

% Tested using Octave 3.2.4 with optim 1.0.15 add on package installed on Windows XP Service Pack 2

% Author: John F. McGowan, Ph.D.

% Copyright (C) John F. McGowan

%

disp('fitting seven (7) Cauchy-Lorentz model to gold price data');

fflush(stdout);

% fit model to gold price data

%floating_gold_price has inflation adjusted gold price since 1970

floating_years = years(71:end);

% Define gold price model functions

% model as linear combination of seven (7) Cauchy-Lorentz (aka Breit-Wigner) functions

leasqrfunc = @(x,p) p(1) ./(1 + (x - p(2)).^2/p(3)^2) + p(4) ./(1 + (x - p(5)).^2/p(6)^2) + p(7) ./(1 + (x - p(8)).^2/p(9)^2) + p(10) ./(1 + (x - p(11)).^2/p(12)^2) + p(13) ./(1 + (x - p(14)).^2/p(15)^2) + p(16) ./(1 + (x - p(17)).^2/p(18)^2) + p(19) ./(1 + (x - p(20)).^2/p(21)^2);

leasqrdfdp = @(x, f, p, dp, func) [1.0 ./(1.0 + (x - p(2)).^2/p(3)^2), (2*p(1)*(x-p(2)))./(p(3)^2*((x-p(2)).^2/p(3)^2+1).^2), (2*p(1)*(x-p(2)).^2)./(p(3)^3*((x-p(2)).^2/p(3)^2+1).^2),1.0 ./(1.0 + (x - p(5)).^2/p(6)^2), (2*p(4)*(x-p(5)))./(p(6)^2*((x-p(5)).^2/p(6)^2+1).^2), (2*p(4)*(x-p(5)).^2)./(p(6)^3*((x-p(5)).^2/p(6)^2+1).^2),1.0 ./(1.0 + (x - p(8)).^2/p(9)^2), (2*p(7)*(x-p(8)))./(p(9)^2*((x-p(8)).^2/p(9)^2+1).^2), (2*p(7)*(x-p(8)).^2)./(p(9)^3*((x-p(8)).^2/p(9)^2+1).^2),1.0 ./(1.0 + (x - p(11)).^2/p(12)^2), (2*p(10)*(x-p(11)))./(p(12)^2*((x-p(11)).^2/p(12)^2+1).^2), (2*p(10)*(x-p(11)).^2)./(p(12)^3*((x-p(11)).^2/p(12)^2+1).^2),1.0 ./(1.0 + (x - p(14)).^2/p(15)^2), (2*p(13)*(x-p(14)))./(p(15)^2*((x-p(14)).^2/p(15)^2+1).^2), (2*p(13)*(x-p(14)).^2)./(p(15)^3*((x-p(14)).^2/p(15)^2+1).^2),1.0 ./(1.0 + (x - p(17)).^2/p(18)^2), (2*p(16)*(x-p(17)))./(p(18)^2*((x-p(17)).^2/p(18)^2+1).^2), (2*p(16)*(x-p(17)).^2)./(p(18)^3*((x-p(17)).^2/p(18)^2+1).^2),1.0 ./(1.0 + (x - p(20)).^2/p(21)^2), (2*p(19)*(x-p(20)))./(p(21)^2*((x-p(20)).^2/p(21)^2+1).^2), (2*p(19)*(x-p(20)).^2)./(p(21)^3*((x-p(20)).^2/p(21)^2+1).^2)]

wt1 = ones(size(floating_gold_price)); % same weight for all data points

t = floating_years; % years when gold price floats

data = floating_gold_price; % inflation adjusted gold price

F = leasqrfunc;

dFdp = leasqrdfdp; % exact derivative

dp = [50.0; 1.0; 1.0; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0 ; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0; 50.0; 1.0; 1.0];

pin = [500.0; 1980.; 5.0; 500.0; 2010.0; 5.0; 500.0; 1982; 2.0; 500.0; 1987; 2.0; 500.0; 1995; 5.0 ; 500.0; 1974; 5.0; 500.0; 1974; 5.0 ];

stol=0.01; niter=100;

minstep = [10.0; 0.2; 0.2; 10.0; 0.2; 0.2; 10.0; 0.2; 0.2; 10.0; 0.1; 0.1; 10.0; 0.1; 0.1; 10.0; 0.1; 0.1; 10.0; 0.1; 0.1];

maxstep = [100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0; 100.0; 5.0; 5.0];

options = [minstep, maxstep];

disp(size(t));

disp(size(data));

disp(size(wt1));

fflush(stdout);

figure(1);

global verbose;

verbose = 1;

[f1, p1, kvg1, iter1, corp1, covp1, covr1, stdresid1, Z1, r21] = ...

leasqr (t, data, pin, F, stol, niter, wt1, dp, dFdp, options);

%

% make a prediction

figure(2);

pred_years = [1970:2020];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (7 Cauchy Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

figure(3);

pred_years = [1970:2050];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (7 Cauchy Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

%

disp('plotting figure 4');

fflush(stdout);

figure(4);

pred_years = [1970:2100];

prediction = leasqrfunc(pred_years, p1);

plot(floating_years, data, 'o', pred_years, prediction, '-');

title('Inflation Adjusted Gold Price (7 Cauchy Prediction vs Data)');

xlabel('Year');

ylabel('Gold Price USD (2009)');

disp('computing final results...');

fflush(stdout);

% C suffix for Cauchy Lorentz model

data_7C = data;

model_7C = leasqrfunc(floating_years, p1);

diff_7C = model_7C - data_7C;

chisq_7C = diff_7C' * diff_7C;

disp('all done');

% THE END

The derivatives of the models with respect to parameters were computed with the symbolic manipulation package Maxima. Maxima was also used to generate some of the Latex mathematical formulas in this article.

Excellent post! With the advent of Quantitative Finance and the Big Data fever, it is really important to think about the limits of Mathematical Modelling.